"Today we have partners (both private and government) & a strong in-house team who collaborate, conceptualize and develop innovative solutions for enabling direct benefit transfers, outcome-driven governance, financial inclusion, rural transformation, health & nutrition, cashless payments, capacity building and agri-business development using technology. We conduct detailed research to understand and analyse factors that could result in greater adoption of digital services and as a result, help improve the quality of life for the poor”.

CDFI partners with various Central/State Ministries/Departments, Govt. institutions, donor institutions, final mile institutions and tech start-ups to develop and implement its solutions across the country.

Latest Updates

Mobile & Web-based solution for ASHA payments.

12:23Bringing transparency & reducing delays in payments to ASHA workers...

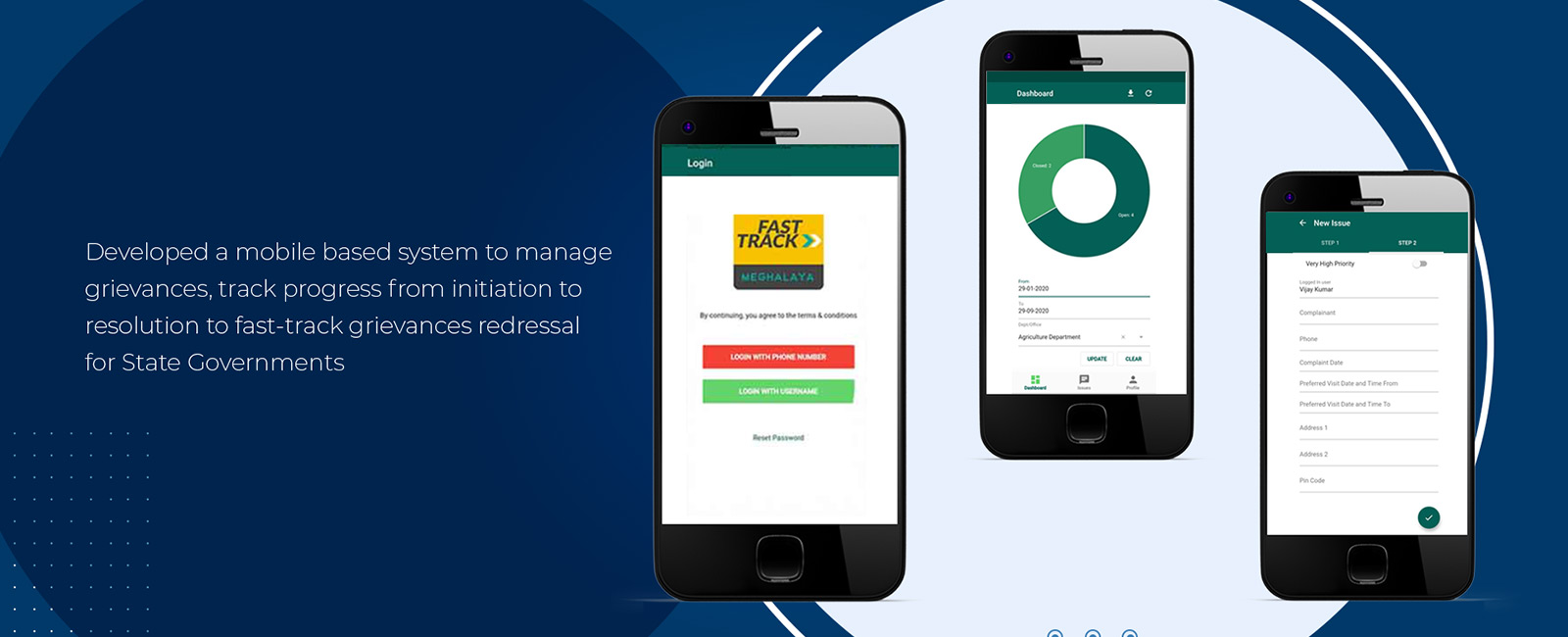

Video on tracking maternal & child care tracking in Meghalaya

12:23How CDFI is enabling Meghalaya Government...

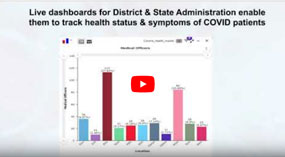

Video on CDFI’s COVID Tracking System in Meghalaya

12:23 CDFI's COVID Tracking System

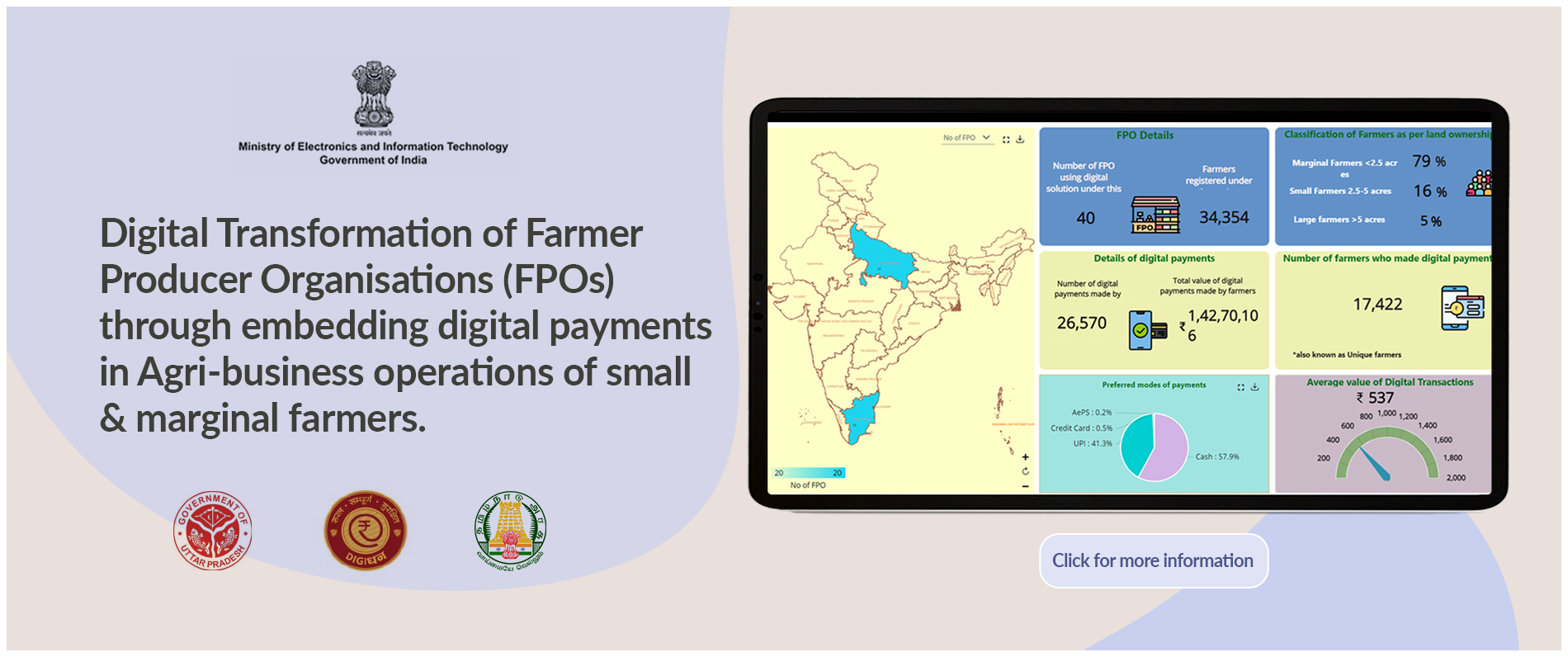

Leaflet on platform for managing agri-business operations of FPOs

12:23 Mobile & web based platform for FPOs...

CDFI's key solutions & Impact achieved

12:23Key solutions & impact achieved across various intervention areas...